At 4:47 p.m., the processor report finally lands, and the reconciliation still isn't ready for review. You don't have a ledger problem yet. You have a source-file problem, and if you want to reduce reconciliation bottlenecks without losing control, that is where the work has to start.

The familiar story is that reconciliation slows down because reviewers are overloaded. Sometimes that's true. More often, the reviewer is waiting on work that should have arrived in reviewable form: source tied to calculation, treatment tied to history, exceptions separated from routine items, and a clear path from support to GL.

Key Takeaways:

- Reconciliation bottlenecks usually begin before review, in the collection, normalization, coding, and support-prep work upstream of the ledger.

- The workpaper is the control surface. It has to show source, calculation, accounting treatment, exceptions, and reviewer sign-off in one place.

- Exceptions are not failures of automation. Missing statements, balance changes, mixed activity, and inconsistent coding belong in front of an accountant.

- Sage Intacct and QuickBooks Online should remain the system of record while preparation happens upstream.

- The safest path is controlled iteration: start with a recurring workflow, compare to a known answer, capture corrections, and expand only after the output is reviewable.

Why Reconciliation Bottlenecks Start Before Review

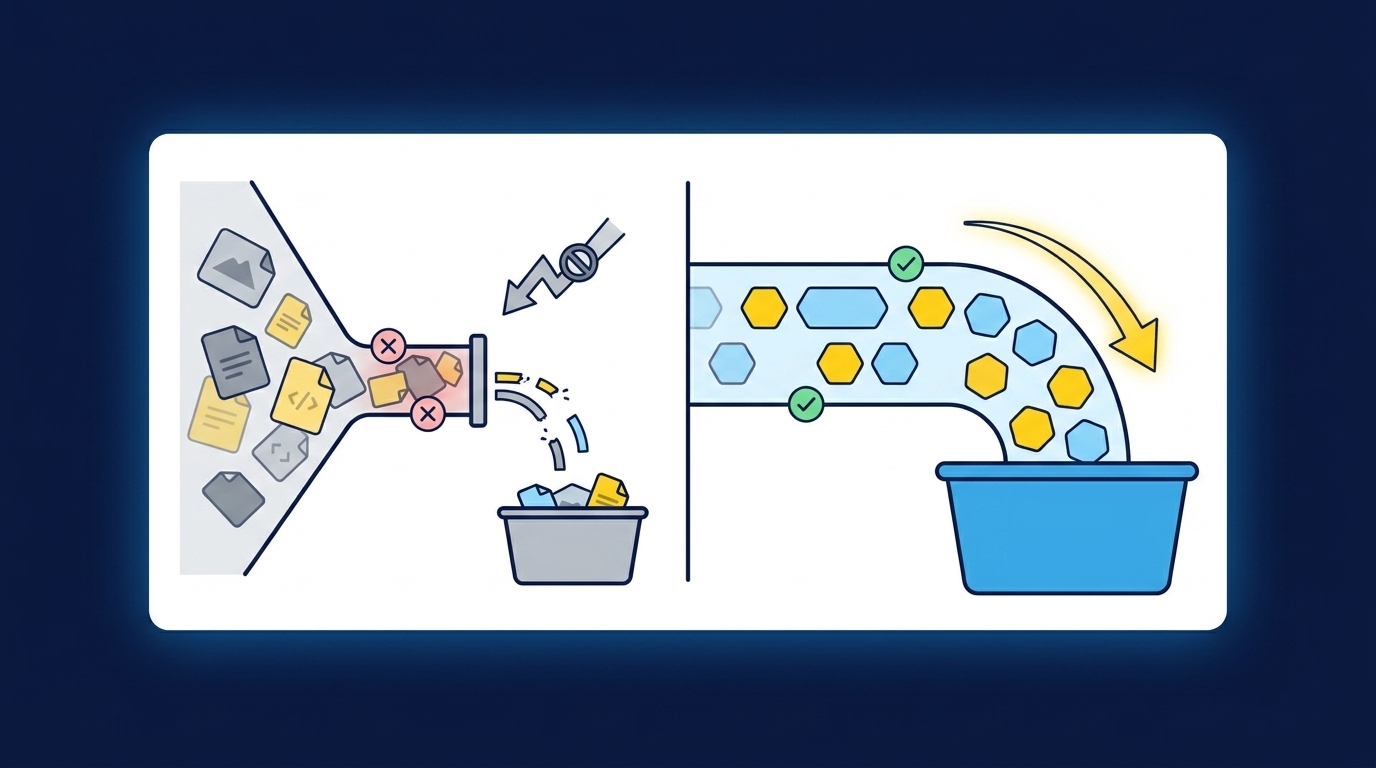

Reconciliation bottlenecks start when source material arrives in formats your team can't use without rework. The ledger may be current, but the supporting work isn't ready. Processor exports, donor reports, bank activity, custodian statements, and prior workpapers all describe related activity in different ways.

The bottleneck is source preparation, not the ledger

Open the close checklist and the delay is always in the review column, so that is where fingers point. The reviewer looks like the constraint because the review column is where the delay becomes visible. In practice, the delay usually began three days earlier, when a senior associate opened a Stripe CSV at 9:12 on a Tuesday morning, found the settlement columns had shifted since last month, and started rebuilding the workpaper in Excel from scratch. By the time the file reached the reviewer, half the close window was already spent on re-typing.

A nonprofit controller sees this every month. The donor platform export has campaign names, the payment processor report has settlement batches, and the bank feed has deposits net of fees. None of those files is wrong. They just don't speak the same accounting language. Before a reviewer can ask whether the treatment is right, someone has to connect the activity, apply fund or program coding, check timing differences, and prepare the support schedule.

That is why clean API feeds don't solve the whole problem. Bank feeds land in neat rows. The rest of the close arrives as PDFs, spreadsheets, portal downloads, and reports that changed layout since last period. The work is more like tying out a binder than loading a table: every tab has to support the one after it, and one missing statement can weaken the whole package.

Here is a diagnostic you can run tomorrow. Time the first sixty minutes your preparer spends on the reconciliation. If more than forty of those minutes go to file cleanup, format matching, prior-period lookup, and manual coding, the bottleneck sits upstream of review. If fewer than twenty, your problem really is reviewer capacity. Anything in between usually means both, and you should fix the source-file layer first because it feeds the reviewer layer. For teams trying to see what upstream preparation can look like before the reviewer touches the file, See Truewind in action in the context of that source-to-workpaper handoff.

Exceptions belong in front of the reviewer

Exceptions get treated like evidence that automation isn't ready. I think that gets the issue backwards. A missing custodian statement, an unexpected balance change, mixed personal and business activity, or a classification that doesn't match prior treatment is exactly the kind of thing a reviewer should see. Hiding it inside a clean-looking reconciliation is the mistake.

The old spreadsheet process has one advantage that is worth respecting: accountants know where they made the call. A reviewer can see the note, the yellow highlight, the copied email, or the tab someone added at midnight. Messy, yes. Visible, though. Any better process has to preserve that visibility, not replace it with a polished output that skips the reasoning.

A practical test is simple. If a preparer can't explain why an item was coded differently from last period, it shouldn't be treated as routine. If a file is missing, the workflow should stop that thread and ask for judgment. If totals don't tie across systems, the output should show the difference instead of forcing agreement. That is not slower. It is control.

Clean-looking output is the real risk

The scary output isn't the one that is obviously wrong. The scary one is the reconciliation that looks complete but doesn't show how it got there. Reviewers don't just need a number. They need to trace the number back to source, inspect the calculation, understand the accounting treatment, and see which exceptions were left open.

That is where a lot of generic AI conversations miss the accounting work. The question isn't whether a model can summarize a statement or propose a category. The question is whether the prepared work can survive a reviewer asking, "Where did this number come from, why is it treated this way, and what did we do last time?" If the answer lives in a prompt history or a disconnected spreadsheet, the reviewer still has to redo the work.

The emotional cost is real, too. Nobody enjoys re-performing a reconciliation because the first version looked fine but didn't show its support. You lose trust in the process, then you lose time checking everything twice. By the second or third month, the team stops asking whether automation is useful and starts asking whether it created another review burden. If your reviewers are re-performing more than one in five reconciliations, the preparation layer isn't ready — no matter how good the summary looks.

How to Reduce Reconciliation Bottlenecks Without Losing Control

To reduce reconciliation bottlenecks without weakening review, move preparation upstream and make the workpaper the center of the process. The workflow should collect source files, apply known accounting logic, separate exceptions, and hand the reviewer an artifact they can inspect. Judgment stays with the accountant.

Start with one recurring workflow that already has a known answer

Pick a workflow where your team already knows what good looks like. A donation reconciliation, processor settlement, brokerage rollforward, prepaid schedule, or fixed asset rollforward is a better starting point than a one-off cleanup project. You want prior-period workpapers, source files, reviewer notes, and posted entries. Without those examples, the workflow has no operating context.

The first run shouldn't be judged by whether it feels impressive. It should be judged against a known answer. Take last period's source files and prior workpaper, prepare the output again, and compare the result to what the team actually signed off. Frankly, this is less exciting than a demo with perfect sample data. It is also the only test that matters.

A useful first workflow has four traits:

- It repeats every period: The same account, source type, or reconciliation returns often enough for corrections to matter.

- It has prior support: The team can supply workpapers, entries, and reviewer notes from earlier closes.

- It has clear ownership: One reviewer owns the accounting treatment and can confirm or correct the output.

- It contains real exceptions: Missing files, timing differences, and classification edge cases are present, not edited out.

That last point matters more than people expect. If the pilot only includes clean files, you learn very little. The test is whether the workflow can prepare the routine work and route the judgment items, in the same format your reviewer already trusts.

Treat the workpaper as the review interface

A workpaper is not a report. It is source, calculation, accounting treatment, exceptions, and reviewer sign-off in one place, in that order. When a reconciliation bottleneck gets reduced without losing control, the reviewer isn't accepting an answer. The reviewer is inspecting prepared work.

That distinction changes the whole process. A report tells you what the output is. A workpaper shows how the output was built. The reviewer can trace a bank deposit back to a processor batch, see the fee treatment, inspect the fund or program allocation, and decide whether an exception needs adjustment. Nothing important is trapped outside the review surface.

A strong workpaper answers five questions before it asks for approval:

- Which source files produced each line?

- What calculation or match created the balance?

- What accounting treatment was applied?

- Which items did not fit the learned pattern?

- Who reviewed, corrected, or approved the output?

Some teams prefer spreadsheet review, and that is a fair preference when the volume is small and the preparer knows every exception by memory. The limitation shows up when multiple preparers touch the same recurring work, or when a reviewer has to re-create context from email and prior files. At that point, the spreadsheet isn't the control. The workpaper logic is.

When the review artifact is the real constraint, a product walkthrough is most useful if it follows the reviewer from source to exception to sign-off rather than starting with a feature list. That is the right moment to Book a Truewind demo, because the question is not whether AI can generate output. The question is whether the output is reviewable.

Normalize inputs before coding decisions begin

Coding too early creates rework. If donor exports, processor reports, bank feeds, and prior workpapers haven't been matched into one preparation flow, the team ends up coding fragments instead of accounting for the activity. One person codes the deposit. Someone else allocates the fees. A third person checks restrictions or entity treatment later. By then, the reconciliation has already split into multiple mini-workpapers.

The better sequence is intake first, structure second, treatment third. Bring the recurring files together, identify what each file represents, match related activity across systems, and only then apply account mappings, dimensions, allocations, or journal-entry treatment. It sounds basic. In close work, basic sequencing is where days are lost.

A family office example makes the point. Custodian statements may include trades, dividends, interest, management fees, and entity-specific activity across multiple vehicles. The statement format may vary by custodian and period. If the team starts by extracting fields, they still have to determine which entity owns the activity, how the prior period treated similar items, and which balances need reviewer attention. Extraction is not preparation.

The diagnostic is straightforward. If your preparer has to open last month's file to remember how to treat the current file, your process depends on memory. If the same mapping, cutoff, or allocation rule is applied every period but lives only in a spreadsheet tab, your process is repeatable in theory and fragile in practice. Put those rules into the preparation flow before coding starts.

Use prior-period logic without freezing judgment

Prior-period workpapers are not just old files. They are evidence of the team's accounting process. They show how accounts were mapped, which cutoffs applied, how exceptions were handled, and where the reviewer changed the preparer's work. That history should shape current-period preparation, but it shouldn't trap the reviewer in last month's answer.

The line is important. A learned workflow should apply known treatment to recurring activity and show where the current period differs. It should not change policy on its own, invent a new allocation, or bury a changed classification because last period looked similar. Accounting judgment moves through the reviewer. The preparation layer just brings forward the context.

One accounting firm described the impact of getting this right in plain terms: "Truewind automates a huge chunk of that busywork." In the same conversation, the point was not that bookkeeping became trivial. The point was that recurring categorization work stopped consuming the same attention every period, which created room for review, client service, and higher-value projects.

There is a real downside here. If your prior workpapers are inconsistent, the first few cycles will expose that inconsistency instead of hiding it. That can feel uncomfortable. It is still useful. The cleanup creates a better operating record, and reviewer corrections become part of the next period's context rather than disappearing into a one-time file.

Route exceptions by decision type, not by file type

A good exception queue is not a junk drawer. It should tell the reviewer what kind of decision is needed. Missing support is different from an unreconciled amount. A new vendor classification is different from a fund allocation change. Mixed activity is different from a timing difference. If all of those land in one pile, the reviewer still has to triage the work by hand.

Route exceptions by the decision they require. Completeness issues go to the person who can obtain the missing statement. Accounting treatment issues go to the reviewer who owns policy. Mapping issues go to the person responsible for chart or dimension logic. Material differences get separated from routine variance. Not glamorous. Very effective.

A workable exception taxonomy can stay simple:

- Completeness: Missing statement, missing export, incomplete support, or unreadable file.

- Tie-out: Bank, processor, donor, custodian, or ERP totals don't agree.

- Classification: Account, fund, program, entity, or department treatment differs from history.

- Allocation: A split rule changed, lacks support, or needs reviewer approval.

- Judgment: The item requires accounting treatment, not clerical resolution.

The hidden benefit is reviewer attention. When exceptions are sorted by decision type, senior accountants spend less time hunting for the issue and more time deciding what to do. That is the real capacity gain. Not fewer accountants. Less clerical fog before judgment begins.

How the Platform Prepares Reviewable Accounting Work

The platform role is to prepare accounting work upstream of the GL while leaving review and approval with the accountant. Source files become structured inputs, known treatment is applied, exceptions are surfaced, and approved output moves to Sage Intacct or QuickBooks Online only after sign-off.

Source files become prepared workpapers

Truewind starts with the source materials the finance team already receives: bank activity, credit-card statements, processor reports, donor-platform exports, custodian statements, prior workpapers, and operational exports. It structures those inputs into workflows that feed reconciliation, coding, schedule preparation, and workpaper generation. The point is not to move files around. The point is to prepare the work in the format the reviewer expects.

That preparation uses the team's existing account mappings, classifications, cutoffs, allocations, and prior corrections as operating context. A processor settlement can be matched against the bank, fees can be separated, dimensional coding can be preserved, and exceptions can be handed to the accountant with source context. A buyer put the review experience bluntly: "Categorization is accurate, and we stopped having to double-check everything." Treat that as a customer statement, not a universal promise. The mechanism is what matters: source, treatment, exception, review.

The same pattern applies to rollforwards and schedules. Prior workpapers, current-period files, and ERP balances feed a review-ready workpaper. Balances roll forward, supporting schedules update, and journal-entry drafts can be prepared with source-linked support. If an item doesn't fit the learned process, it is surfaced for review rather than forced into the closest category.

Reviewer sign-off controls the push to the GL

Truewind does not replace Sage Intacct or QuickBooks Online. Those systems remain the source of truth. Preparation happens upstream, and the accountant reviews the workpaper, confirms or adjusts treatment, and signs off before structured output moves into the GL. That boundary is not a technical footnote. It is the control model.

The review surface shows source links, exception queues, and reviewer actions. Corrections are captured against the workflow so later periods can reflect confirmed treatment without changing policy on their own. The audit trail preserves the path from source file to coding decision to reviewer approval, which means a questioned workpaper can be inspected instead of reconstructed from email.

One customer conversation captured the larger point better than a feature description: "It's not just about making bookkeeping simpler; it's about freeing up teams, and helping them focus on higher-value projects." Another buyer said, "If I had to describe Truewind in one word: Lifechanging." Strong words, worth treating as one buyer's experience rather than a blanket claim. The practical takeaway is narrower and more useful: when preparation is repeatable and review stays in the loop, the team can spend more time on the exceptions that actually need accounting judgment. If that is the workflow you want to inspect, Get a Truewind demo after you choose the reconciliation or rollforward you would test first.

Keep the Ledger as the Source of Truth

The path forward is not autonomous posting or a new ledger. It is controlled preparation before the ledger: source files organized, known treatment applied, exceptions separated, workpapers made reviewable, and accountants kept in charge of sign-off. That is how finance teams reduce reconciliation bottlenecks without weakening the close.

Start with one recurring workflow. Use the prior-period answer as the benchmark. Ask whether the prepared workpaper shows source, calculation, treatment, exceptions, and reviewer approval clearly enough that the reviewer can accept or correct it without rebuilding the file. If it does, expand. If it doesn't, fix the review surface before adding more volume.

What goes away is not the accountant. What goes away is the pile of clerical preparation that used to sit between source documents and judgment.

Frequently Asked Questions

How do I handle edge cases effectively?

To manage edge cases effectively, start by ensuring that your workflow includes a clear taxonomy for exceptions. For instance, categorize issues by decision type, such as completeness, classification, or allocation. This way, you can route each exception to the appropriate person for resolution. Additionally, using Truewind's proactive anomaly detection can help surface these edge cases early, allowing your team to address them with the necessary context. By focusing on the specific nature of each exception, you can streamline the review process and maintain control over your accounting outputs.

Can I automate data ingestion for my reconciliation process?

Yes, you can automate data ingestion using Truewind. Start by uploading your raw source materials, such as bank statements, credit card activity, and other financial documents. Truewind will then convert these messy inputs into structured workflows, which reduces the manual effort typically required for data preparation. This automation helps you begin the reconciliation process more efficiently, ensuring that your data is organized and ready for further accounting tasks without the usual delays.

What if my source files have inconsistent formats?

If your source files come in inconsistent formats, Truewind can help by standardizing these inputs during the ingestion process. When you upload your documents, Truewind organizes the data into a structured format, making it easier to work with. This way, you can focus on the reconciliation and review processes rather than spending time on manual formatting. By ensuring that your data is consistent, you can significantly reduce the bottlenecks that often arise from mismatched file formats.

How do I ensure my team maintains control over the review process?

To maintain control over the review process, utilize Truewind's Human-in-the-Loop Review Workflow. This feature allows accountants to inspect prepared workpapers and reconciliations before any outputs move downstream. By ensuring that every item is reviewed and approved by a designated accountant, you can capture corrections and maintain a clear audit trail. This process not only preserves accountability but also enhances the accuracy of your financial reporting.

When should I use prior-period workpapers in my current reconciliation?

You should use prior-period workpapers when preparing your current reconciliation to establish a baseline for what good looks like. This practice helps you apply known accounting treatments and identify any discrepancies in the current period. Truewind facilitates this process by allowing you to reference past workpapers and source files, ensuring that your current outputs align with established standards. This approach not only enhances consistency but also provides a framework for addressing any exceptions that arise.

Turn this into a close-ready workpaper

Start with sample files or upload your own statements to see how Truewind prepares review-ready workpapers and journal entries.